China's Laser Industry: Global Leader and Cluster Development

source:

keywords:

Time:2025-06-16

In recent years, China's laser industry has witnessed vigorous development and achieved remarkable achievements, leaping to become one of the core forces in the global market and demonstrating strong vitality and huge potential.

I. Market Scale: Half of the Global Market with Strong Growth Momentum

China's laser market features a rich and diversified structure, covering multiple segments such as laser processing equipment, optical communication devices and equipment, laser measurement equipment, laser generators, laser medical equipment, and laser components. Among them, the laser processing equipment market accounts for the largest share, with rapid development speed and enormous future market potential.

According to statistics, the output value of China's laser industry was approximately 98 billion yuan in 2023, with a market scale of nearly 100 billion yuan, accounting for more than 50% of the global laser equipment market share. It is expected that the sales revenue of laser equipment in China will reach 110 billion yuan in 2024. During the "Golden Decade" development period, the sales scale of China's industrial laser generators and systems has maintained an average annual growth rate of over 16% in the past decade, showing a strong growth trend.

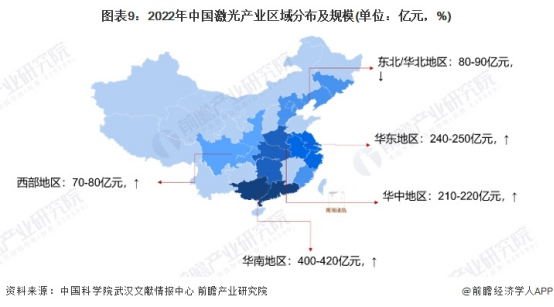

II.Regional Distribution and Industrial Clusters

The development of China's laser industry shows obvious regional concentration characteristics, forming multiple industrial clusters mainly distributed in the Pearl River Delta, Yangtze River Delta, Central China, and the Bohai Rim region. Cities such as Shenzhen, Wuhan, Suzhou, and Jinan have become representatives, jointly outlining China's "laser territory."

Shenzhen

Guangdong, Jiangsu, and Hubei have the most complete industrial chains. The centralization of enterprises in South China, East China, and Central China is high, with relatively complete industrial chains, and their laser output values rank among the top in the country.

According to research data from the Forward Industry Research Institute in 2023, as of the end of 2023, Guangdong Province had 26,958 laser and related enterprises, ranking first; Jiangsu Province had 13,818, ranking second; Hubei Province had 9,997, ranking third; and Shandong Province had 8,093, ranking fourth.

Wuhan Optics Valley

The Pearl River Delta mainly produces medium and low-power laser processing equipment. Relying on its flexible market mechanism and complete manufacturing supporting facilities, it occupies an advantage in the medium and low-power field.The Yangtze River Delta focuses on high-power laser cutting and welding equipment. Backed by a strong industrial foundation and scientific research strength, it has achieved remarkable results in high-power applications.The Bohai Rim region is dominated by high-power laser cladding equipment and all-solid-state laser devices, with unique advantages in the R&D and production of high-end laser devices.Central China covers most high, medium, and low-power laser processing equipment, with strong industrial comprehensiveness.

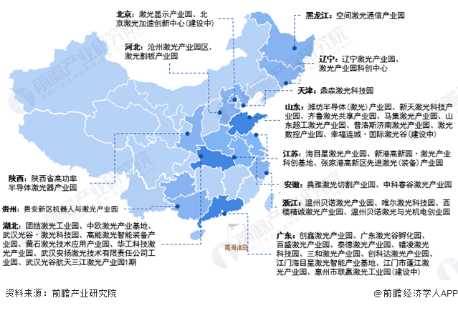

Key Regions of China's Laser Industry

Central China (represented by Wuhan): Relying on the scientific research resources of Huazhong University of Science and Technology and other universities, it has established a complete industrial chain covering R&D, devices, equipment, and applications, with a national - leading technological density.

Pearl River Delta Region (represented by Shenzhen): Driven by the precision processing of consumer electronics, it has gathered leading enterprises such as HAN'S LASER, with outstanding market - oriented application capabilities.

Yangtze River Delta Region (represented by Suzhou): Focusing on the heavy - industry manufacturing scenarios, its high - power welding equipment technology has reached the international advanced level.

Emerging Regions: The Sichuan - Chongqing region (new - display laser), Shaanxi (optical communication devices), and Northeast China (accelerating the formation of a 10 - billion - level supporting cluster).

Suzhou

From the perspective of laser industrial parks, as of 2023, there are 54 large-scale laser industrial parks in China, mainly distributed in Shandong, Guangdong, Hubei, Liaoning, Zhejiang and Jiangsu. Among them, Shandong has the largest number with 12, followed by Guangdong with 11, Hubei with 9, Liaoning and Zhejiang with 4 each, and Jiangsu with 3. Beijing, Hebei, Anhui and Shaanxi each have 2, while Tianjin, Heilongjiang and Guizhou each have 1.

III.Industry Chain: Upstream, Midstream and Downstream Collaborate, with Remarkable Breakthroughs in Localization

(I) Upstream

The upstream of the laser industry chain mainly includes light source materials, optical components, and other materials composing lasers. Representative enterprises include Suzhou JCZ Laser, CASTECH, AFR, Suzhou Everbright Photonics, Focuslight Technologies Inc., etc. These enterprises continuously invest in the R&D and production of light source materials and optical components, providing a solid foundation for the manufacturing of midstream laser devices.

(II) Midstream

The Chinese laser device market started relatively late, but domestic enterprises have achieved large-scale production of laser devices and core optical components by breaking through core technologies. This has promoted the decline in the cost of optical raw materials and triggered an explosive growth in the capacity of domestic laser equipment. Representative enterprises in the midstream include RAYCUS, MAX PHOTONICS, Shenzhen JPT Opto-electronics, Shanghai BOCHU Electronic Technology Company Limited, BWT, Suzhou Everbright Photonics, X Photonics, etc. They continue to strive for performance improvement and cost control of laser devices, enhancing the market competitiveness of domestic laser devices.

(III) Downstream

As a major manufacturing country, China's huge demand has given birth to numerous downstream manufacturers in the laser industry, involving multiple fields such as laser processing, optical communication, optical storage, laser medical treatment, laser marking, laser typesetting and printing, laser measurement, laser display, etc. Typical representatives in the downstream include UW Laser, HAN'S LASER, GBOS LASER INC, Hgtech, DCT, bodor, GWEIKE, TIANHONG LASER, Yawei, Shenzhen Sunshine Laser, GOLDEN LASER, etc. They apply laser technology to various industries, promoting the transformation and upgrading of traditional manufacturing.

IV. Development Status in Other Regions

Other regions in China, such as the West and Northeast, also have potential for laser industry development. Western regions like Shaanxi, Sichuan, and Chongqing have initially formed a relatively complete laser industry supporting system with a wide range of industry categories, involving new displays, optical communication, lasers, LED lighting, photovoltaics, application-based optoelectronic terminals, etc. The laser industry in Northeast China, including Liaoning and Jilin, has developed rapidly in recent years, introducing and cultivating a number of excellent laser enterprises, such as Dalu Laser, Shenyang Jinyan Laser, Yongli Laser, etc.

Xi'an High-tech Zone

In general, China's laser industry has made remarkable progress in market scale, regional distribution, and the completeness of the industry chain. In the future, with continuous technological innovation and the expansion of application fields, China's laser industry is expected to maintain rapid growth and play a more important role in the global laser market.

9th Secret Light Awards Launch: Million-Yuan Fund + National Award Recommendation

9th Secret Light Awards Launch: Million-Yuan Fund + National Award Recommendation Top Enterprises Gather: 1st Laser & Additive Manufacturing Innovation Conference Wraps Up

Top Enterprises Gather: 1st Laser & Additive Manufacturing Innovation Conference Wraps Up 2025 ams OSRAM Explorer Conference: "China Engine" Drives Future Innovation

2025 ams OSRAM Explorer Conference: "China Engine" Drives Future Innovation Tsinghua's Sun Hongbo, SLA Review Expert, Becomes CAS Academician

Tsinghua's Sun Hongbo, SLA Review Expert, Becomes CAS Academician 4th Collaboration! What Brought the Global Laser Academic Guru to Chinese Univs & Leading Firms?

4th Collaboration! What Brought the Global Laser Academic Guru to Chinese Univs & Leading Firms? Scanner Optics: Galvanometer Tech Leader

Scanner Optics: Galvanometer Tech Leader The "Light Chasers" in the Deep Ultraviolet World

The "Light Chasers" in the Deep Ultraviolet World Shi Lei (Hipa Tech): Focus on Domestic Substitution, Future Layout in High-End Laser Micromachining

Shi Lei (Hipa Tech): Focus on Domestic Substitution, Future Layout in High-End Laser Micromachining Optizone Technology: 17 Years Devoted to Optics – High-Power Optics Mass-Production Pioneer

Optizone Technology: 17 Years Devoted to Optics – High-Power Optics Mass-Production Pioneer Zhuojie Laser: Breaking barriers via tech breakthroughs, aiming to lead high-end light sources

Zhuojie Laser: Breaking barriers via tech breakthroughs, aiming to lead high-end light sources